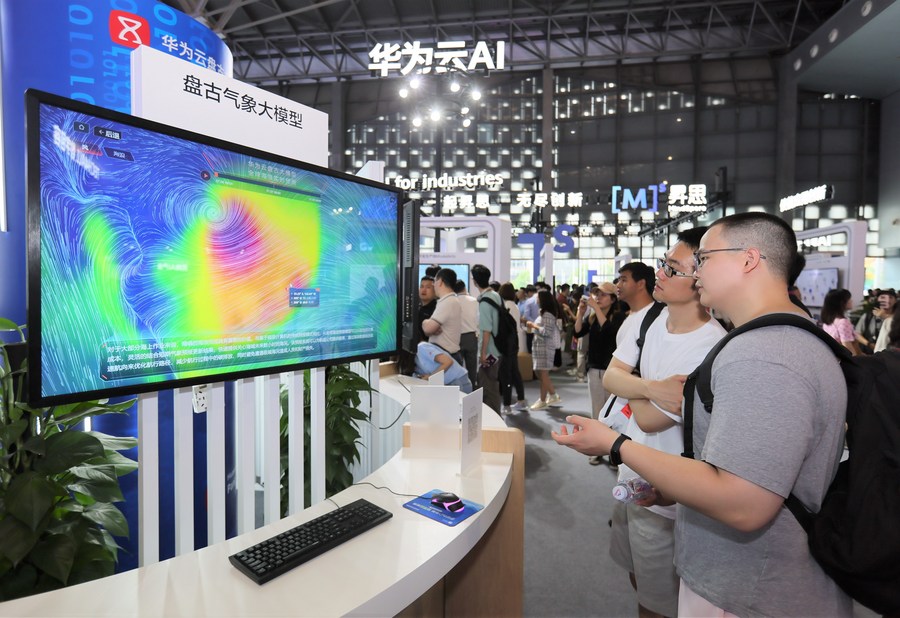

BEIJING: China has revealed its first artificial intelligence (AI) model designed to analyse the impact of weather patterns on financial markets, marking a novel step in climate-aware risk management, Xinhua reported, citing the China Meteorological Administration (CMA).

The model Shangji, or Stock, was jointly developed by the Shanghai-based Fudan University and the National

Meteorological Information Centre. Its core function is to assess how meteorological factors influence asset pricing, offering a new tool for investment decisions and financial risk assessment, the CMA was quoted as saying by Science and Technology Daily yesterday.

Zhao Yanxia, a lead developer of the model and director of the CMA key open laboratory for financial meteorology, said by utilising global reanalysed meteorological data and historical stock trading data, the model is able to forecast short-term returns for the majority of stocks on China’s A-share market.

Validation tests indicate that the model is capable of accurately identifying industries highly sensitive to weather conditions, such as wind and solar power, traditional petrochemicals, construction, and agriculture, thereby aligning with international standards.

Back-testing of investment strategies based on the model’s predictions has shown “sustained and stable positive returns” over various historical periods, suggesting practical potential, Zhao explained.

The model holds broad application prospects in the financial sector, said Li Hao, a professor at the Artificial Intelligence Innovation and Incubation Institute of Fudan University and one of the model’s creators.

Companies in weather-sensitive industries can use it for climate risk management, while banks and insurers can apply it to control risks in businesses such as equity pledges and explore climate-related financing, Li noted.

Li added that the model is useful for investors as an aid in quantitative investing, and that academics can employ its output to test and refine asset pricing theories.

The research team plans to expand the model’s scope to include bonds and futures, aiming to continuously update it to keep pace with market dynamics. – BERNAMA-XINHUA