“I am all in a sea of wonders. I doubt; I fear; I think strange things, which I dare not confess to my own soul.”

– Dracula (1897) by Bram Stoker (1847-1912), Irish novelist

MY teenage daughter Bella, newly obsessed with the world of finance thanks to a programme called Rock the Street, Wall Street (RTSWS), reached out the other night to share what she’d learned.

“Guess what we covered today?” the math geek asked, as if she couldn’t believe it herself.

“We covered scams,” she said, “and also… Bram Stoker.”

For the next twenty minutes or so, she talked nonstop about Dawn, a mathematician from Soros Fund Management who had led the session.

What stayed with her wasn’t the charts or forecasts, but a killer line: “Fraudsters are vampires without the elegant evening attire and romantic backstories.”

The analogy holds well. Like Dracula, a fraudster must be invited in, mentally rather than physically, before they can drain your bank account.

“That’s how the bite happens,” she said, half amused, half deadly serious.

This column offers some talismans to ward them off.

Unfortunately, garlic does not work on human bloodsuckers.

Fraud is a huge international criminal business.

It has transcended its cottage industry roots due to the internet.

Crooks can contact almost anyone, anywhere.

The data we scatter on social media helps them target us.

Deepfake technology likewise.

Politicians and bankers are freaking out.

Fraud is denting public confidence in the financial system.

Four years ago, my top commodities analyst, Hannah, launched a project called ‘Stop! Think Fraud’ out of personal interest.

It aims to bolster consumers’ resistance to authorised push payment (APP) fraud.

These cons depend on us, the hapless mugs, saying “yes” to money transfers between our bank and a fraudster’s account.

APP fraud is proliferating.

It has many attractions for evil criminals.

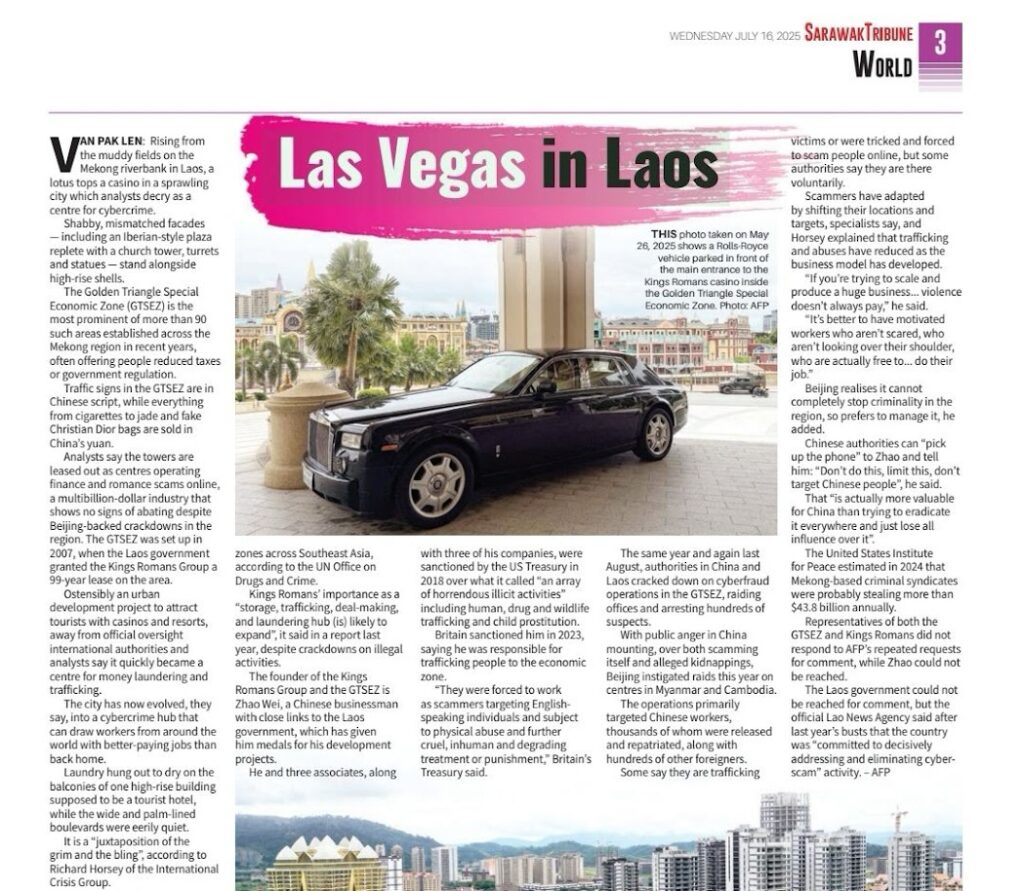

Coincidentally, I had just published an insightful AFP feature, ‘Las Vegas in Laos’ on July 16, detailing a slick scam operation that wouldn’t look out of place in a Michael Mann movie.

Several details stood out to me, as they mirrored ‘routines’ typically known only in investment banking.

Meaning, they use data and behaviour prediction, similar to how a banker might model market scenarios or hedge risk.

So the very next day, I sent Hannah in to investigate further.

There’s a model I’ve been trying to close for years and this might be the missing link.

These fraudsters are unlikely to get caught, as armed robbers often are.

They do not have to build supply chains of the kind needed for drug trafficking.

Staff costs are low; their workers may be enslaved migrants.

Best of all, APP fraud capitalises on the mental biases that most humans possess.

Truth bias is the big one, as the late economist Daniel Kahneman explained in ‘Thinking, Fast and Slow’.

“This is our tendency to believe what people tell us,” I recall him saying in a lecture, though, at the time, I barely grasped what he meant.

Truth bias has common sense underpinnings, he added: “Most of the time, people tell us what is true. When it is not, they have generally made a mistake rather than lied.”

The moment when you metaphorically put out a “welcome” mat for Nosferatu is when your truth bias nudges you into believing a fake scenario.

For three years, I worked with Hannah and a few others from J.P. Morgan modelling elaborate frauds – the digital shell games, the disappearing funds, the too-good-to-be-true projections.

We could spot a scam from a mile away.

But like the shoemaker’s children who go barefoot, we never thought to model the part where I’d end up chasing payment for our work.

On the bright side, though, I’m glad those models are now informing enforcement actions.

Our findings show that the two main types of APP fraud rely on fabricated scenarios.

In fast frauds, which are often for modest stakes, the fraudster aims to panic you into believing in an invented emergency.

He is a teenage relative, overseas, broke and texting, asking for cash.

She is a tax official, trying to forestall a police raid on your dwelling.

Urgency precludes second thoughts.

It denies you time to check identities.

Fast frauds remind me of a phenomenon I encountered in diver training known as “the incident pit”.

A flood of adrenaline can kill you rather than save you in an underwater emergency, I learnt.

Terrified, the victim reacts chaotically, worsening the crisis.

Trainers teach scuba noobs and real emergency workers the mantra: “Stop, think, act”.

It helped me in a couple of tight spots.

The title of Hannah’s anti-fraud project echoes this formula.

Presented with a scenario that rattles you, put down the phone or step away from the computer.

Think for a minute.

Is the scenario a likely one?

Ask the person contacting you whether it is okay to disconnect.

Can you get back to them via a verifiable phone number or email?

Do they mind if you take advice from a smart third party?

If “no” is the answer to those questions, you are being scammed.

Bail out and report what happened to your bank.

Slow frauds are usually more sophisticated and involve higher stakes.

The fraudster grooms the victim into accepting the fake scenario as a prolonged reality rather than a brief crisis.

So-called “romance” and investment scams are commonest.

Here, the scammer creates a scenario the victim welcomes rather than fears: an attractive potential partner or a lucrative get-rich-quick scheme.

The investment scammer typically sets up a bogus website purporting to show your money multiplying.

“The fraudsters prey on the endowment effect,” Hannah said.

The endowment effect is a cognitive bias where people place a higher value on things they own simply because they own them, even if the item has no real increase in utility or value.

Scammers exploit this bias by making you feel like money or a prize is already yours, perhaps through fake investment returns, lottery wins, or inheritance scams. Once you believe it’s yours, you become more emotionally attached and more likely to make irrational decisions (like paying a “processing fee”) just to avoid losing that illusionary gain.

“You do not want to lose that money.”

The crook will warn of a wipeout if you do not stake more or if you ask to take gains.

You should not send money in the first place.

Instead, you should try to verify the identity of the business, bailing out if you fail.

The company should have a registration with a reputable regulator.

It should have a website with a credible address and a helpline number that is not answered immediately by someone who already seems to know who you are.

You should also run the proposed investment past a smart third party.

Friends and relatives can often spot scams more easily than the targets.

They are not emotionally invested in a scenario being true.

The advice of a Singapore-based senior investment banker is to “break the spell”: wriggle free from the fake scenario before you believe it fully.

Last October, we made parties responsible for reimbursing victims of APP fraud up to $85,000, subject to some exclusions.

Victims will still have to cope with shame and embarrassment.

The daughter of a mutual friend was scammed out of several thousand dollars by a fraudster impersonating her boss.

She had recently joined the workforce and feared losing her job.

“They are very clever at targeting you psychologically,” she said, “I felt very stupid afterwards.”

You may live in a quiet village where the worst peril is a person on a runaway bicycle.

You may feel confident that criminals cannot break into your home.

But they do not need to, when so many of us invite them into our heads.

Reserve willing suspension of disbelief for trips to the theatre.

When money is involved, doubt is the best default.

The views expressed here are those of the columnist and do not necessarily represent the views of Sarawak Tribune. The writer can be reached at med.akilis@gmail.com