CHINA’S recent export controls on six rare earth elements (REEs) and rare earth magnets have sent the world in a tizzy.

These products are used for several applications ranging from cleantech to weapons.

The electric vehicle industry is hardest hit, giving out stress signals that many factories can even shut down if China doesn’t loosen the curbs.

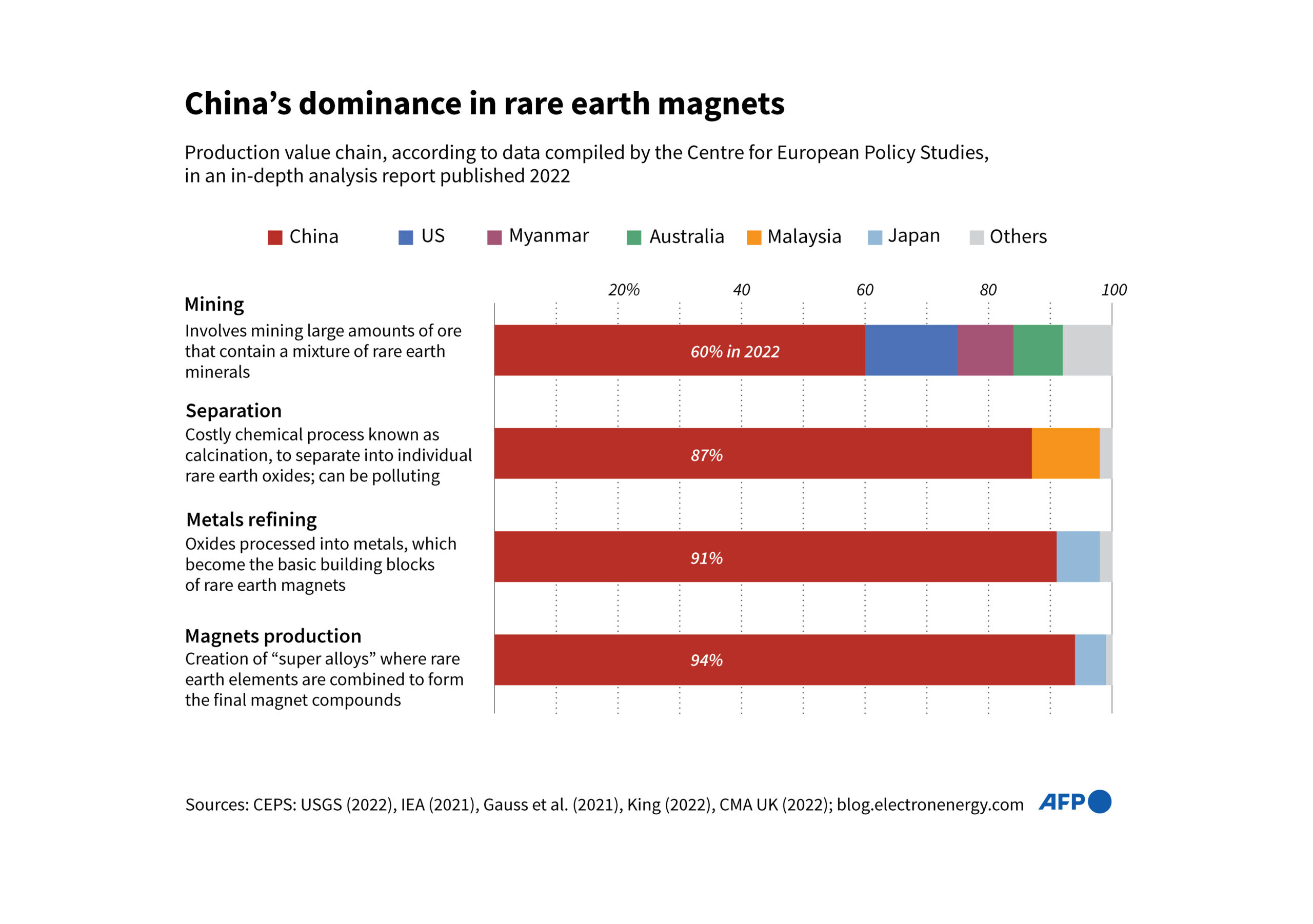

The global supply chain for these elements is heavily dependent on China, which currently accounts for about 70 per cent of the world’s mined REEs and roughly 90 percent of refined production.

China also produces nearly 90 per cent of the world’s rare earth magnets used in vehicles.

Although these curbs are not a complete ban on exports for the auto sector, companies must now seek prior government approval before shipping these materials out of China.

This adds uncertainty and delay in the supply process.

China’s strategic use of rare earths as an economic weapon may offer short-term leverage, but it can run into risks in the long run.

China may be controlling the present of rare earths, but it may not control their future.

The myth of rarity of rare earths

The term “rare earth elements” (REEs) is a misnomer.

Comprising 17 metallic elements—including neodymium, dysprosium, and praseodymium—these materials are relatively abundant in the Earth’s crust.

Cerium, for example, is more common than copper.

What makes them “rare” is the difficulty in finding them in economically viable concentrations and the even greater challenge of separating them from each other, as they tend to occur in clusters.

Commercial deposits are spread across the globe—from Australia and the US to India, Brazil, and parts of Africa.

Yet, almost all of global rare earth refining still happens in China.

This isn’t due to a lack of resources elsewhere; it’s the result of decades of strategic policy decisions by Beijing and complacency from the rest of the world.

How China monopolised rare earths

China’s dominance in the rare earth industry is not geological — it is geopolitical.

Beginning in the 1980s and accelerating through the 1990s, China deliberately cultivated rare earth mining and refining as a strategic industry.

It offered subsidies, low-cost loans and lax environmental regulations, allowing it to undercut Western producers who were burdened by stricter standards and higher costs.

By the early 2000s, China had effectively driven many competitors out of business.

The Mountain Pass mine in California, once the world’s leading rare earth producer, was shuttered in 2002 due to both economic and environmental pressures.

This left China not only as the dominant supplier of rare earth elements but also as the global refinery for turning them into usable materials for magnets, batteries and electronics.

In effect, China monopolised the middle and downstream segments of the value chain—where the true economic and strategic value lies.

Refining and processing, not mining, is where pricing power, technological influence, and geopolitical leverage are concentrated.

China’s rare earths move can backfire

Since many countries have rare earths deposits as well as the capability to refine them, China’s gambling on a rare leverage it has on the world.

Having spent eight years tracking China’s rare earths metrics, I’ve seen how it applies pressure selectively and then steps back but a hard stance will only cost it dearly.

By restricting rare earth exports, China aims to pressure foreign industries and governments, especially those pushing back against its strategic and technological ambitions.

This tactic, however, is not without risks, as reflected in the scenarios I presented in April.

Firstly, this weaponisation creates powerful incentives for other countries to invest in their own rare earth infrastructure.

The US, Europe, Japan, Australia and India have already begun allocating significant resources to rebuild rare earth supply chains.

Australia’s Lynas Rare Earths has ramped up production, and the US government has designated rare earths as critical minerals, channelling funding toward domestic refining capabilities.

India is expediting steps to boost domestic availability of critical minerals.

Changes to the Mines and Minerals (Development and Regulation) Act are being fast-tracked.

Besides regulatory tweaks, the centre is also expecting commercially viable domestic production of rare earth permanent magnets in small quantities later this year.

After the fourth meeting of the India-Central Asia Dialogue (between US investment banks and state officials) held in New Delhi last week, India and five central Asian countries have expressed interest in joint exploration of rare earths and critical minerals.

India is also working on alternate sources for magnets derived from rare earth minerals, commerce and industry minister Piyush Goyal said while speaking to my analysts in Germany a few days ago.

“In a way, it’s a wake-up call for all those who have become over-reliant on certain geographies. It’s a wake-up call for the whole world that you need trusted partners in your supply chain,” the minister said.

On alternative sources, the minister said these could also be some technologies that India is developing.

“The government, the industry and startups and innovators are all working as a team and we are confident that there may be a problem in the short run but we will emerge winners in the mid to long runs,” he said.

China’s move will surely accelerate innovation in material science.

Companies are increasingly investing in rare-earth-free alternatives, such as ferrite magnets or advanced electric motor designs that reduce or eliminate the need for REEs.

Long-term, this could shrink global dependence on rare earths altogether, diminishing China’s leverage.

Once other countries begin producing their own rare earths and develop technology to produce magnets as well as alternatives, China will start losing export markets and also its leverage on other countries.

Much of its rare earth industry is export-oriented, particularly in the high-value-added processing and magnet manufacturing sectors.

As buyers diversify or localise supply chains, Chinese producers could find themselves facing overcapacity and declining global relevance.

The current disruption may well be a turning point.

What is happening is not just a scramble for resources, but a deeper strategic pivot.

Countries are beginning to view rare earths not as a commodity, but as a national security asset.

Governments are deploying industrial policy driven by private sectors, economic incentives and international cooperation to ensure secure and sustainable access.

In the short term, China’s dominance in refining will continue to cause pain for sectors dependent on these inputs such as electric vehicles.

But in the medium to long term, the very act of leveraging this dominance could cause its erosion.

Chinese rare earth monopoly will fracture under the weight of its own power play.

It’s possible that China soon eases export curbs since it knows the risk of overplaying its hand.

But the world has realised China’s intent to weaponise critical supply chains and it will keep trying to break its China dependence.

The views expressed here are those of the columnist and do not necessarily represent the views of Sarawak Tribune. The writer can be reached at med.akilis@gmail.com